P.S. Free & New 8011 dumps are available on Google Drive shared by ITExamSimulator: https://drive.google.com/open?id=1fotYrR3nNSU0ITXcKPqZQH_dEiNY39cu

For most people who have no much time to prepare the PRMIA real exam, latest 8011 exam questions will be your excellent partner to help you get high passing score in the valid test. Once you receive our 8011 Dumps Torrent, it will just need one or two days to practice test questions and answers. If you finished it well, clearing exam will be easy.

To prepare for the PRMIA 8011 CCRM certificate exam, candidates need to have a background in finance, statistics, accounting or an equivalent degree. It is also advisable to go through the PRMIA official study materials and attend PRMIA approved training or workshops to improve their understanding of the certification exam’s topics. Passing the exam requires dedication, determination, and hard work, but obtaining the CCRM certification can significantly enhance a risk manager's career prospects.

PRMIA 8011 Certification Exam is a rigorous exam that requires a significant amount of preparation and study. 8011 exam consists of 100 multiple-choice questions and is three hours in length. To pass the exam, individuals must achieve a score of at least 70%. 8011 exam is administered at Pearson VUE testing centers around the world, making it accessible to individuals in many different locations.

Before you buy our 8011 study questions you can have a free download and tryout and you can have an understanding of our 8011 exam questions by visiting our pages of our 8011 learning guide on the website. The pages of our 8011 guide torrent provide the demo and you can understand part of our titles and the form of our software. So before your purchase you can have an understanding of our 8011 Exam Questions and then decide whether to buy our 8011 study questions or not.

The Professional Risk Managers' International Association (PRMIA) is a non-profit organization that offers globally recognized certifications in risk management. The PRMIA 8011 (Credit and Counterparty Manager (CCRM) Certificate) Certification Exam is designed to validate the knowledge and skills of professionals in the field of credit and counterparty risk management. 8011 Exam covers a wide range of topics, including credit analysis, credit risk mitigation, counterparty risk management, and regulatory compliance.

NEW QUESTION # 111

All else remaining the same, an increase in the joint probability of default between two obligors causes the default correlation between the two to:

Answer: C

Explanation:

The default correlation between two obligors goes up if the joint probability of default between them increases. This is intuitive. Also consider the formula for the default correlation between two obligors Default correlation = [P(1,2) - P1 * P2] / #P1*(1-P1)*P2*(1-P2); where P(1,2) is the joint probability of default between the two and P1 and P2 are their individual probabilities of default. Obviously, an increase in P (1,2) will cause the default correlation to increase.

NEW QUESTION # 112

Which of the following statements is true in relation to the Supervisory Capital Assessment Program (SCAP):

I. The SCAP is an annual exercise conducted by the Treasury Department to determine the health of key financial institutions in the US economy II. The SCAP was essentially a stress test where the stress scenarios were specified by the regulators III. Capital buffers calculated under the SCAP represented the amount of capital that the institutions covered by SCAP held in excess of Basel II requirements IV. The SCAP focused on both total Tier 1 capital as well as Tier 1 common capital

Answer: A

Explanation:

In the February of 2009, the Federal Reserve (which is the US central bank system) and other US banking regulators embarked on a simultaneous assessment of the capital held by the 19 largest US bank holding companies. This was an unprecedented exercise of a kind never undertaken before, and was known as the Supervisory Capital Assessment Program (SCAP). The purpose of the exercise was to determine the amount of additional capital (called the 'capital buffer') each of the institutions covered would need to ensure that it would have sufficient capital if the economy weakened more than was then expected. The idea was that these financial institutions would then raise additional capital equal to their respective capital buffers by the fourth quarter of 2009.

Statement I is false on two counts: firstl the SCAP was conducted by the US central bank and other regulators, and not the 'Treasury Department' (the Treasury Department in the US is the equivalent of the Ministry of Finance in may other countries). Second, the SCAP was a one time exercise, and not annual.

Statement II is correct. The regulators prescribed rates of losses on credit assets of different kinds and other macro-economic assumptions, and asked the banks to determine the extent of losses they would need to bear (in addition to calculating them independently too). Therefore the SCAP was a stress test where the scenario was prescribed by the regulators.

Statement III is false. Capital buffer under the SCAP referred to the additional capital the banks would need to have certain ratios of capital, and not 'excess' capital.

Statement IV is correct. The SCAP envisaged two capital targets: a Tier 1 capital ratio in excess of 6% at the end of 2010; and a Tier 1 common capital ratio in excess of 4%. Therefore both the total Tier 1 capital and Tier 1 common capital were targeted.

Therefore Choice 'c' is the correct answer.

NEW QUESTION # 113

When compared to a medium severity medium frequency risk, the operational risk capital requirement for a high severity very low frequency risk is likely to be:

Answer: C

Explanation:

High frequency and low severity risks, for example the risks of fraud losses for a credit card issuer, may have high expected losses, but low unexpected losses. In other words, we can generally expect these losses to stay within a small expected and known range. The capital requirement will be the worst case losses at a given confidence level less expected losses, and in such cases this can be expected to be low.

On the other hand, medium severity medium frequency risks, such as the risks of unexpected legal claims, 'fat- finger' trading errors, will have low expected losses but a high level of unexpected losses. Thus the capital requirement for such risks will be high.

It is also worthwhile mentioning high severity and low frequency risks - for example a rogue trader circumventing all controls and bringing the bank down, or a terrorist strike or natural disaster creating other losses - will probably have zero expected losses & high unexpected losses but only at very high levels of confidence. In other words, operational risk capital is unlikely to provide for such events and these would lie in the part of the tail that is not covered by most levels of confidence when calculating operational risk capital.

Note that risk capital is required for only unexpected losses as expected losses are to be borne by P&L reserves. Therefore the operational risk capital requirements for a low severity high frequency risk is likely to be low when compared to other risks that are lower frequency but higher severity.

Thus Choice 'c' is the correct answer.

NEW QUESTION # 114

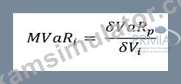

Which of the following best describes the concept of marginal VaR of an asset in a portfolio:

Answer: C

Explanation:

The correct answer is choice 'd'

Marginal VaR is just the change in total VaR from a $1 change in the value of the asset in the portfolio. All other answers are incorrect. Mathematically, it is expressed as follows, where VaRp is the VaR for the portfolio, and Vi is the value of the asset in question.

A mathematical equation with numbers and symbols Description automatically generated

Other answers describe other VaR related concepts such as incremental VaR, Component VaR and Conditional VaR.

NEW QUESTION # 115

Which of the following is the best description of the spread premium puzzle:

Answer: D

Explanation:

Choice 'a' is the correct answer. The other choices represent non-sensical statements.

NEW QUESTION # 116

......

Latest 8011 Braindumps Files: https://www.itexamsimulator.com/8011-brain-dumps.html

BONUS!!! Download part of ITExamSimulator 8011 dumps for free: https://drive.google.com/open?id=1fotYrR3nNSU0ITXcKPqZQH_dEiNY39cu